|

|

Overcoming our love of the co-pay: A case for HSA-qualified plans

Although we don't think most people memorize their health insurance policies from cover to cover, they do tend to have an attachment to some aspects of their coverage. And co-pays are often the part of the coverage that people like the most.

But it makes sense -- co-pays are predictable and manageable, even when life isn't. You pay the copay when you get to the doctor's office, and your insurance picks up whatever the rest of the cost is. You know it's going to cost $XX to go to the doctor, and there are no surprises -- which is really appealing when a busy week gets even busier, thanks to unexpected doctor visits.

The same goes for prescription drugs, or urgent care visits. People like knowing what things cost beforehand, to determine if it's a manageable amount. So, when we start talking about plans that require the patient to pay the full cost of things like office visits, people understandably become worried.

Don't be worried with HSAs

In order to get the tax benefits of contributing to an HSA, you need to have an HSA-qualified high deductible health plan (HDHP). And the IRS has pretty strict rules for HDHPs. Here are just a few of the big ones to know:

- The insurance policy can't pay for anything except preventive care (any services or treatments, such as screenings and immunizations, designed to prevent health problems) before the deductible.

- In 2024, the deductible has to be at least $1,600 if you've got coverage for just yourself, and at least $3,200 for family coverage.

- In 2023, the maximum out-of-pocket can't be more than $8,050 for individual coverage, and $16,100 for family coverage.

The minimum deductibles are actually pretty similar to average deductibles across all plans. Most plans have deductibles these days, and for plans with deductibles, the average deductible for a single employee was more than $1,700 in 2023.

But the part about the HDHP not paying for anything except preventive care before the deductible is what tends to cause stress. You have to pay for everything until you've paid the whole deductible?

No wonder people sometimes decide to skip the HDHP in favor of a more traditional plan with nice, predictable co-pays. But don't dismiss an HDHP without really crunching the numbers. Here are some other points to keep in mind when selecting the right plan for you:

- If you have a choice between a traditional plan with co-pays and an HDHP, how much will you save in monthly premiums if you pick the HDHP?

- How often do you typically go to the doctor or fill a prescription or get other medical services that are covered with a copay?

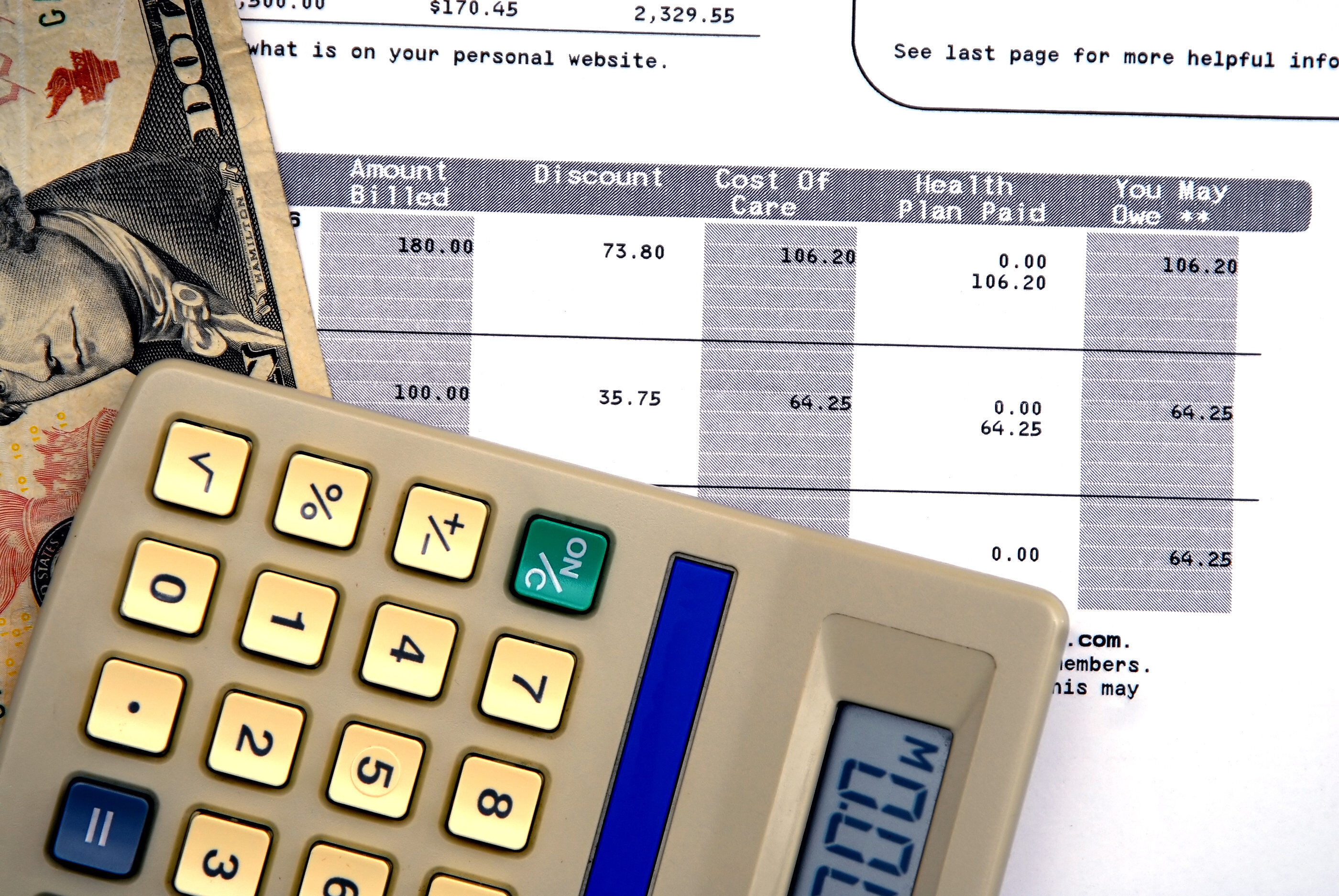

- Take a look at the statements you've received from your insurance company the last few times you went to the doctor or had some other service that was covered with a copay. How much did the insurance company pay on your behalf, in addition to the copay you paid? And how much of the charge was simply eliminated (written off) based on your insurance company's contract with the doctor?

If you get an HDHP, you don't have to pay the full charged amount for medical care before the deductible, you just have to pay the full amount that the insurance contract allows. Your doctor might charge $180 for an office visit, but if the HDHP has a negotiated rate of $115, you'll only have to pay $115 and you will have paid the full price for the visit. (To take advantage of a negotiated rate, participants should follow the guidelines of their plan, such as using in-network providers.)

- Consider the benefits of the HSA itself. If you have HDHP coverage, you can put up to $4,150 into the HSA, tax-free, in 2024. That total is $8,300 if you cover at least one other family member on your HDHP.

Talk with a tax adviser (or use a tax calculator) to see how much an HDHP could save you in taxes — keeping in mind that since the HSA contribution reduces your adjusted gross income (AGI), it might make you eligible for other tax benefits, like premium subsidies if you buy your own health insurance.

Once you take all of that into consideration, you might find that in the long run, you'll come out ahead financially if you pick the HDHP. You just have to look at all the combined financial effects, instead of just comparing the bill you're going to get for an office visit versus the copay you'd have if you picked a more traditional health plan.

,")

,")

★

★

★

★

★

$44.99

-

$51.99

Compare to Caring Mill™ All-Day Allergy Cetirizine Hydrochloride Tablets - 45 ct. at $19.99